Foundational Principles for Prudent Investing

Explore foundational principles for prudent investing, focusing on long-term value, patience, and strategic decision-making for lasting wealth.

Summary

Successful investing hinges on clear rules, deep understanding of few bets, patience, and a business-owner mindset, focusing on long-term value over market noise.

Key Points

- Define investment rules; stick to them.

- Focus on few, well-understood investments.

- Patience and observation yield best results.

Key Takeaways

- Invest like you're buying the whole company.

- Productive assets build long-term wealth.

- Simple, disciplined approaches beat complex strategies.

Definition of Key Terms

- Intrinsic Value: The "true" underlying value of a company or asset, based on its fundamentals such as earnings, assets, and future prospects, distinct from its current market price.

- Dividends: A portion of a company's profits paid out to its shareholders, typically on a per-share basis.

- Stock Split: An action by a company to divide its existing shares into multiple shares, increasing the number of shares outstanding while lowering the price per share proportionally.

- Book Value: The net asset value of a company, calculated as total assets minus intangible assets (such as goodwill) and liabilities. Roughly, what would be left for shareholders if the company liquidated its assets and paid off its debts.

- Market Value: The current total worth of a company's outstanding shares in the stock market, calculated by multiplying the current stock price by the total number of shares.

- Arbitrage: The simultaneous purchase and sale of an asset in different markets or in different forms to profit from a difference in its price. In a broader sense, it can refer to profiting from price discrepancies in situations such as mergers.

- ESOPs (Employee Stock Option Plans): A right given to employees to purchase shares of the company at a predetermined price at a future date. It's a form of compensation.

- EBIDTA (Earnings Before Interest, Taxes, Depreciation, and Amortization): A measure of a company's operating profit before deducting interest, taxes, depreciation, and amortization expenses.

- PBT (Profit Before Tax): A company's profit before corporate income tax is deducted. It includes operating profit and other income, minus interest expenses.

- P/E Ratio (Price-to-Earnings Ratio): A valuation ratio calculated by dividing a company's current share price by its earnings per share (EPS). It indicates how much investors are willing to pay per unit of earnings.

- Index Funds: A type of mutual fund or exchange-traded fund (ETF) with a portfolio constructed to match or track the components of a financial market index, such as the Nifty 50 or BSE Sensex

- Share Buyback (or Repurchase): When a company buys its own outstanding shares from the marketplace, reducing the number of shares available.

- Interest Coverage Ratio: A debt and profitability ratio used to determine how easily a company can pay interest on its outstanding debts. Calculated as Earnings Before Interest and Taxes (EBIT) or Pre-Tax Earnings divided by interest expense.

- Productive Assets: Assets that generate income or returns on their own, such as businesses, rental properties, or farms, as opposed to assets held purely for price appreciation (such as collectibles or some commodities).

Introduction

After spending countless hours reading Warren Buffett's shareholder letters, I'm writing this down to consolidate the wisdom I've gathered. These insights have transformed my understanding of investing. I've distilled them into practical principles that are easy to follow. What you're about to read is grounded with Buffett's real-world experience and success, carefully analyzed to help you build lasting wealth while sleeping soundly at night.

Setting Your Own Rulebook

First things first, you need your own set of investment rules. And here’s the kicker: you must stick to them. Simply put

Define your investment rules and stick to them. Review them if some don't make sense.

This is super important. These rules will be your guide, helping you make decisions when things get confusing or when everyone around you is panicking.

- Write down what makes an investment good for you.

- Consistently apply these rules to every opportunity.

- Don't just set and forget. Every so often, take a look at your rules.

- Do they still make sense?

- Are they working for you?

- If not, it's okay to tweak them.

- The market changes, and your understanding will grow.

The Power of Focus: Quality over Quantity

Don't put all your eggs in one basket?

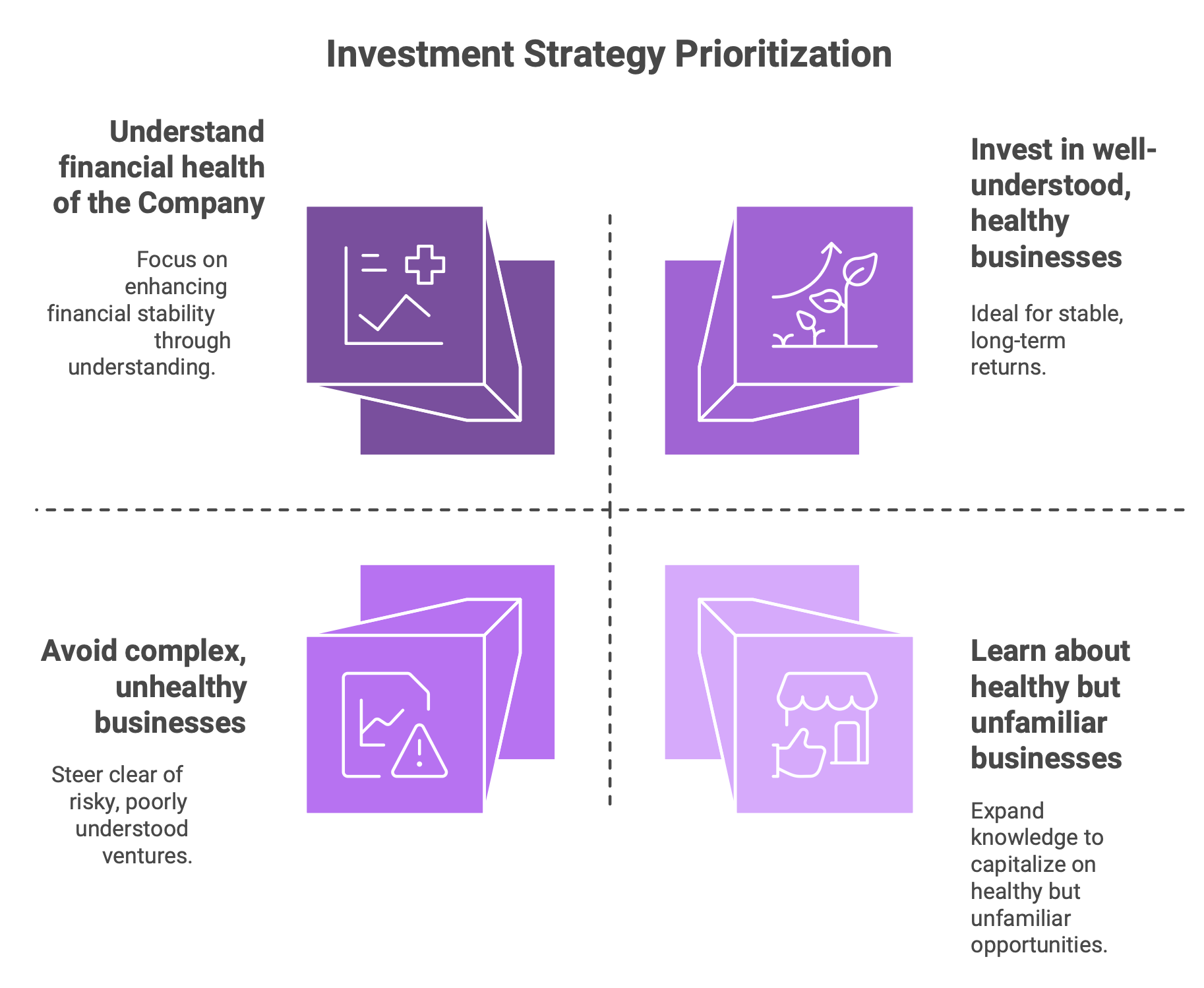

When making investment decisions, diversification has its place but do bear in mind that most people have achieved great long-term returns by focusing on a select few investments. The key is that you must understand these investments inside out and they should have strong fundamentals.

Focus on a few good investments for long-term returns

- Concentrate on businesses you genuinely comprehend. If you can't explain what a company does to a 10-year-old, maybe steer clear for now.

- Look for companies with solid financial health and good prospects.

- Thorough research on a few is better than superficial knowledge of many.

The Virtue of Patience: Let Your Investments Breathe

This might sound a bit overused, but a patient and observant approach often works best.

Passive focus on investments leads to the best results. If the records speak for themselves, avoid asking or involving yourself so that it works best.

If you've picked a good company, trust its performance. Constant meddling can sometimes does more harm than good.

- Once you invest, give your investments time to grow. Think of it like planting a seed; you don’t dig it up every day to see if it’s sprouting.

- Strong company performance will eventually be recognized by the market.

- Avoid the temptation to react to every market rumour or news headline.

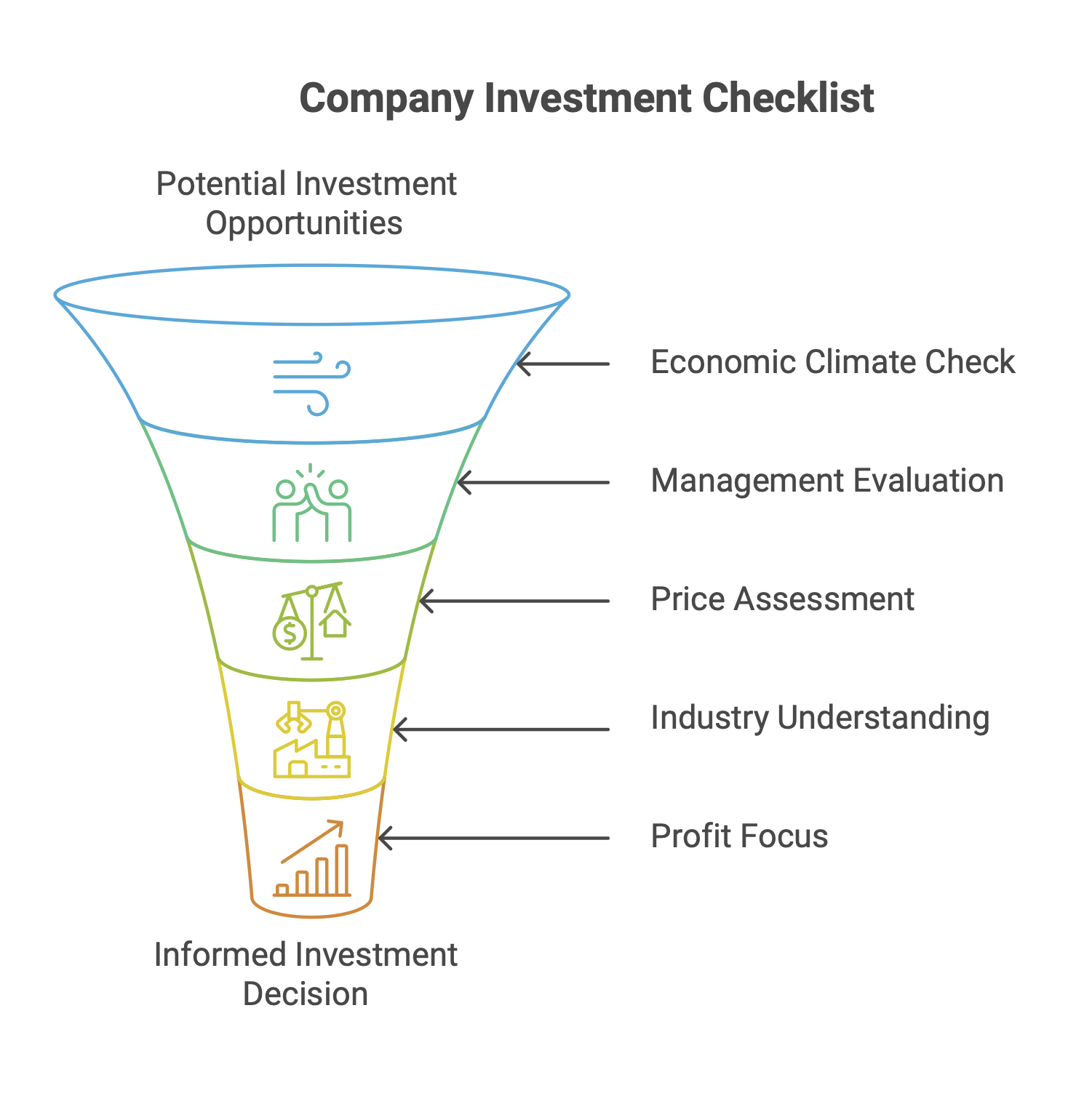

What to Look For: Your Investment Checklist

So, what makes a company worth your hard-earned money? Here’s a simple checklist that will serve as your initial filter before you even consider putting money into a company.

The Big Picture: Economic Scenario

- Is the overall economic climate looking good for this company? You want more tailwinds (things that help) than headwinds (things that hinder).

The People Behind the Scenes: Management

- Is the company run by competent and honest people? This is huge. Good leaders steer the ship well, even in choppy waters.

The Price Tag: Is it a Good Deal?

- Is the purchase price attractive compared to what it would cost to build a similar business from scratch (private ownership value)? You’re looking for a bargain, essentially getting more value than what you’re paying.

Keep it Simple: Understandable Industry

- Is the industry easy to understand? If it’s too complicated, it’s harder for you to judge its future.

Profit Focus: Especially in Private Firms

- If you get a chance to invest in private firms,prefer those with a high focus on profit. They are often keenly managed for returns.

Think Like a Business Owner, Not Just a Stock Picker

This is a golden rule. When you buy a stock, you're buying a piece of a business. So, apply the same logic you would if you were buying an entire company.

- Pro-rata Discount: Often, owning a part of a business (shares) comes at a discount compared to buying the whole thing. These can be excellent long-term investments.

- Bargain Hunting: When the market gets jittery and prices drop for good companies, that’s your cue! Buy small portions of equity at bargain prices when these opportunities pop up. Don’t try to catch a falling knife, but a temporary dip in a solid company can be an invitation.

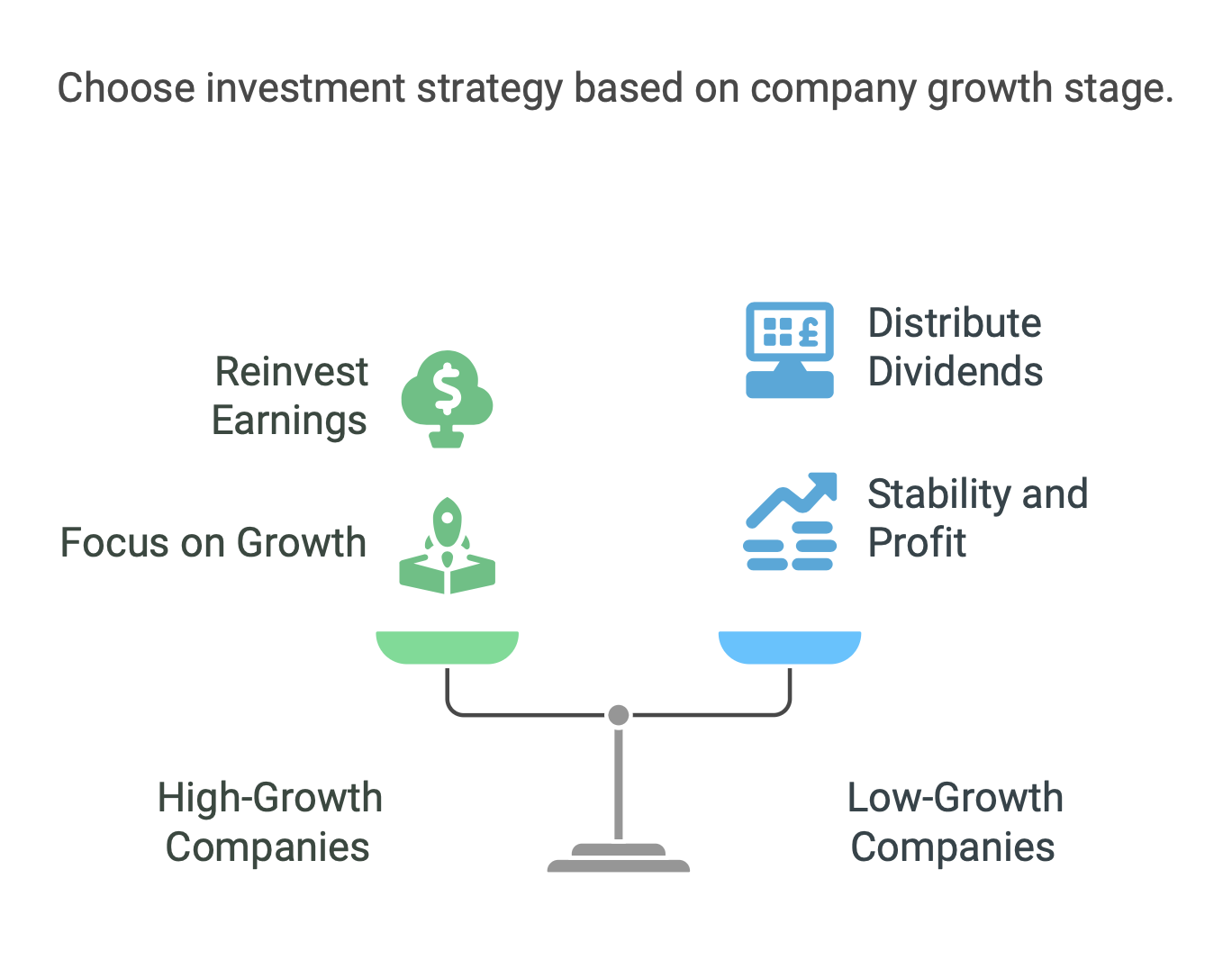

Dividends: The Sweet Bonus

Who doesn’t like a little extra cash? Dividends are a portion of a company's profits paid out to shareholders.

- Focus on companies that pay dividends. Do bear in mind the following:

- For high-growth companies: Rather than paying dividends, these companies retain their earnings (profits they keep) to buy back more shares or invest in new projects, which over time increase the value of your investment.

- For low-growth companies: Many companies generate great profits but find limited use for cash generated, so they prefer to distribute dividends to their investors. Use these dividends to reinvest in other high-growth opportunities.

- Understand if the the dividend are being paid from real profits and not by issuing new shares (which overtime reduce value of your investment).

The Magic of Retained Earnings

Here’s a neat trick: invest in companies where every rupee they keep and reinvest in the business leads to at least a rupee of growth in their market value. This shows the management is using your money wisely to grow the company.

- If a business looks good and is making solid economic profit, consider buying more shares if the price drops due to general market negativity, not because something is wrong with the company itself.

A Note on Stock Splits

You might hear about stock splits, where a company divides its existing shares into multiple shares. For instance, one share of ₹1000 might become ten shares of ₹100.

- Stock splits often lead to increased trading volume. This can cause the share price to move further away from its true underlying value (intrinsic value).

- This is one reason why some very successful investors, such as Warren Buffett, don't generally encourage stock splits for their companies. They prefer investors who are focused on the business's long-term value, not short-term price movements.

The Skewness of Returns: Not All Parts Are Equal

It’s common to see companies, especially large ones, where just one or two divisions are superstars, delivering amazing returns. The other parts of the business might be just average or even subpar.

- On average, the company might still show good returns, but often hides under-performers. This is often played out in companies that grow by acquiring other businesses.

- If you can identify this, the ideal strategy would be to (though almost impossible for individual investors such as ourselves) encourage the company to focus on or spin off the high-performers and fix or sell the under-performers.

How Companies Really Grow

Most companies improve their earnings by using more capital – either by reinvesting their profits or raising more money.

- It's a rare gem that generates so much cash it can invest significantly in completely new, high-return ventures outside its core business.

- Typically, companies increase their value by retaining their earnings and reinvesting them into their existing operations, rather than always finding new high-rate businesses.

Share Buybacks: A Good Sign?

Sometimes, companies use their cash to buy back their own shares from the market.

- If a company's market value is less than its intrinsic (true) value, a share buyback is a smart move. It means the company believes its own stock is undervalued.

- This is good for remaining shareholders because their ownership percentage in the company increases, and they get a larger share of future earnings.

Your Investor Toolkit: Evaluating a Company

Before deciding to invest in a company's stock, put on your business analyst hat, not just a market analyst or security analyst hat. Always bear in mind that you’re assessing the business itself.

The Core Evaluation

- Economic Prospects: What are the future prospects for the business and the industry it operates in?

- Management Quality: How good is the management? Look at their track record. Have they been honest and effective?

- Price: Is the price you’re paying for a share sensible, given the above?

Always aim to buy outstanding businesses at sensible prices. It’s usually better than buying mediocre businesses even if they seem like a bargain.

Book Value vs. Market Value

Keep an eye on the growth of a company’s book value (roughly, what the company’s assets are worth minus its liabilities) compared to its market value (the total value of all its shares).

- However, book value is a historical number. Always consider the company's future prospects too. A company with great future potential might trade at a higher market value compared to its current book value, and that can be perfectly fine.

Three Key Questions Before You Invest

Whenever you're looking at a company, try to answer these:

- What's the company approximately worth? (Your estimate of its intrinsic value).

- How likely is it that the company can meet its future financial obligations? (Is it financially stable?).

- How good a job has the management done, considering the economic conditions they faced?(Compare them to their competitors – are they outperforming, underperforming, or just average?).

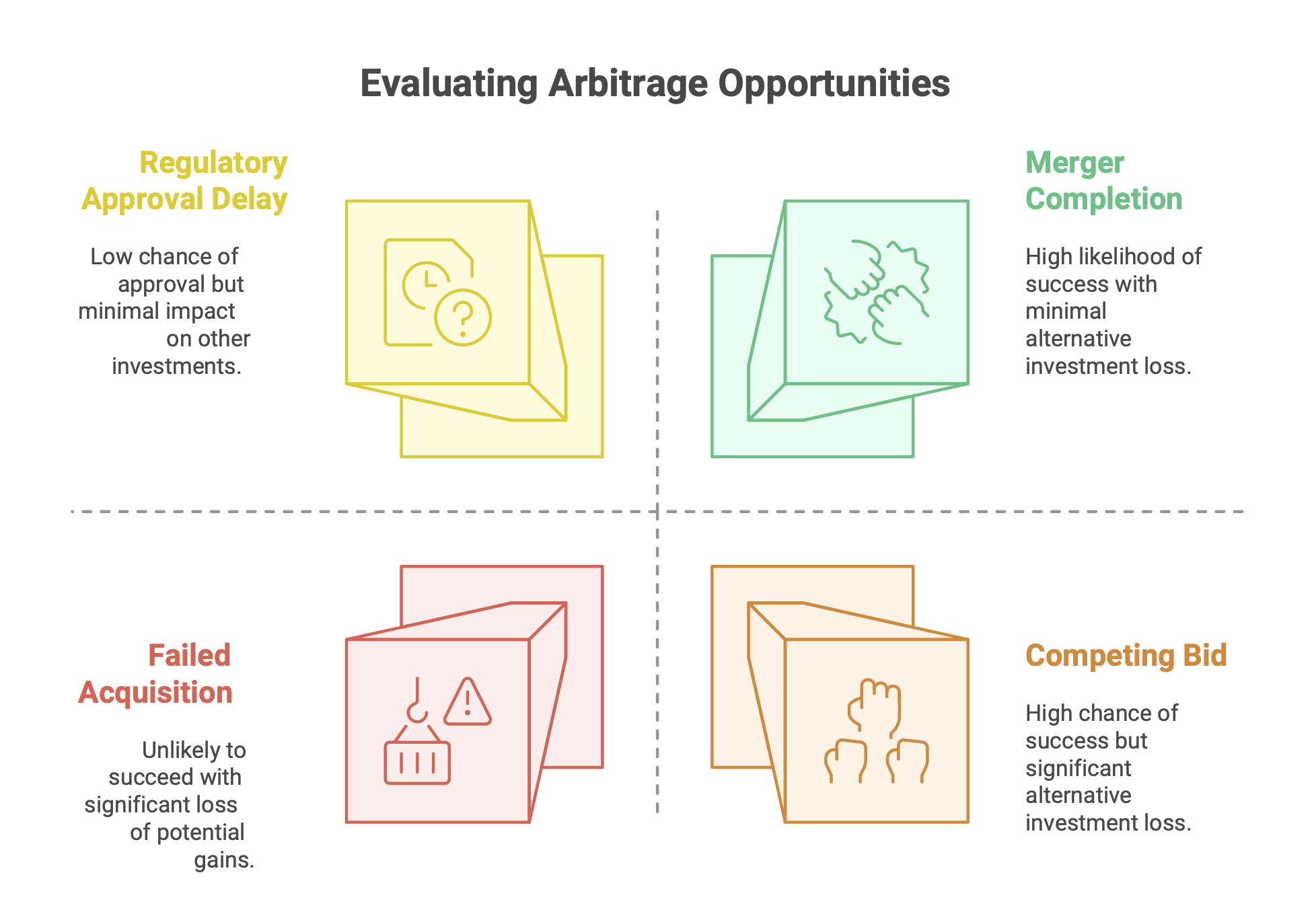

Spotting Arbitrage: The Special Situations

Sometimes, special situations arise in the market, such as when one company announces it's buying another. These can create "arbitrage" opportunities, where you might be able to make a profit with relatively low risk if things go as planned. But tread carefully!

Four Questions for Arbitrage

- What's the probability of the expected event actually happening?

- How long will your money be tied up waiting for this event?

- What are the chances of a better investment opportunity coming along while your money is locked in here? (Opportunity cost).

- What happens if the anticipated event doesn’t occur due to some unforeseen issue? (What's your downside?).

The Market Isn't Always "Efficient"

You might hear about the "Efficient Market Theory," which suggests that stock prices always reflect all available information, making it impossible to beat the market.

- Well, experience shows markets are frequently efficient, but not always. This is where those arbitrage opportunities and chances to find undervalued gems come from.

- There are many examples of individual investors and fund managers who have performed better than the overall market over long periods. How? Not by magic, but by careful evaluation of facts and a disciplined approach. You don’t make money by just committing to a particular investment category or style, but by smart analysis

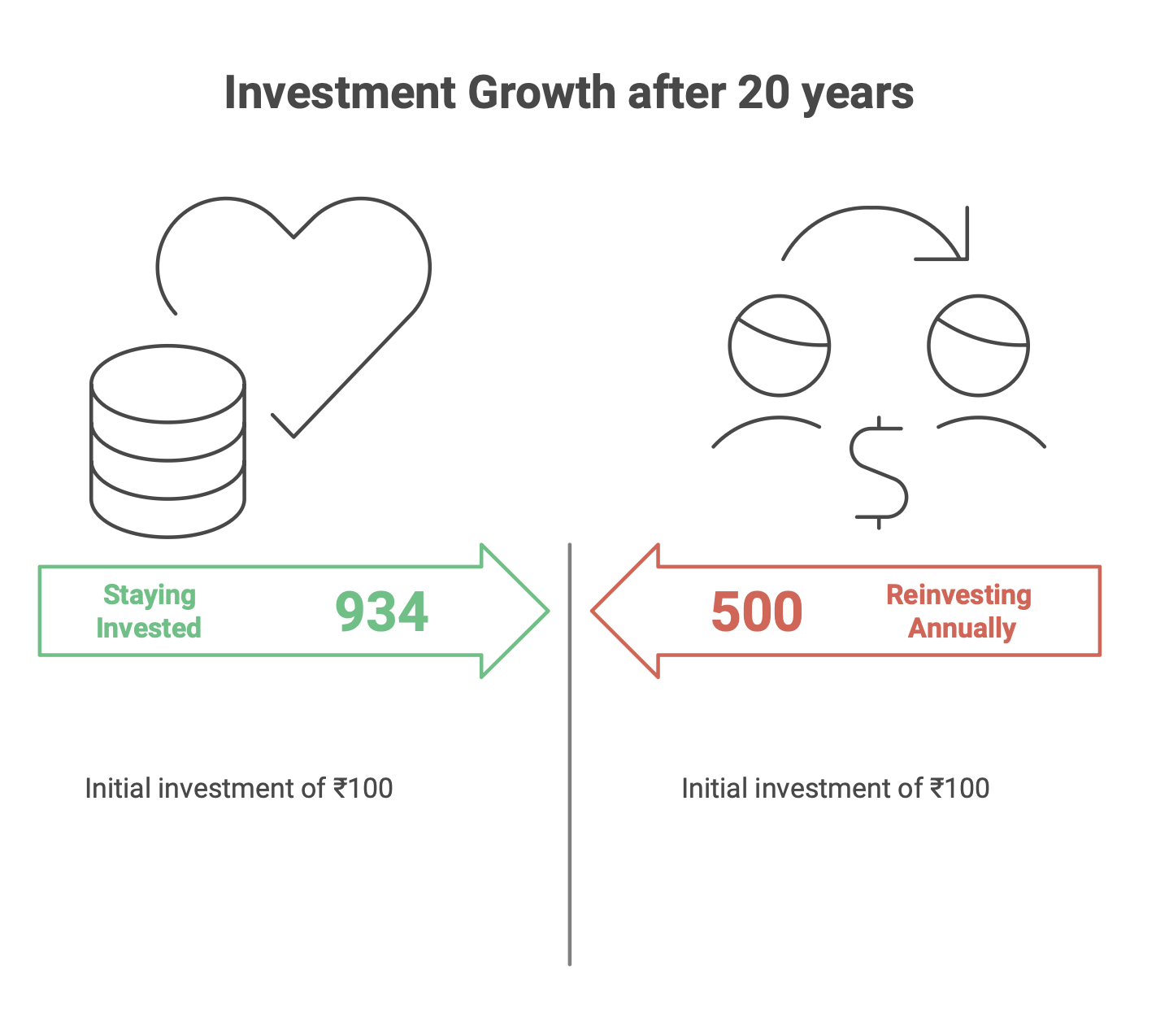

The Magic of Compounding: A Simple Long-Term View

Let me show you why staying invested for the long term can be so powerful. Imagine this:

- Scenario 1: You find an investment that grows by 12.5% every year. At the end of each year, you take out your profits, pay a 30% tax on those profits, and then reinvest what's left. If you do this for 20 years, your initial ₹100 would grow to about ₹500. Not bad.

- Scenario 2: Same investment, 12.5% annual growth. But this time, you stay invested for the full 20 years. At the very end, you sell and pay 12.5% tax on your total profits. Your initial ₹100 would grow to about ₹934!

See the difference? If you're confident in an investment, staying invested allows your money (and the returns on your returns) to compound more effectively, even after taxes. Patience pays!

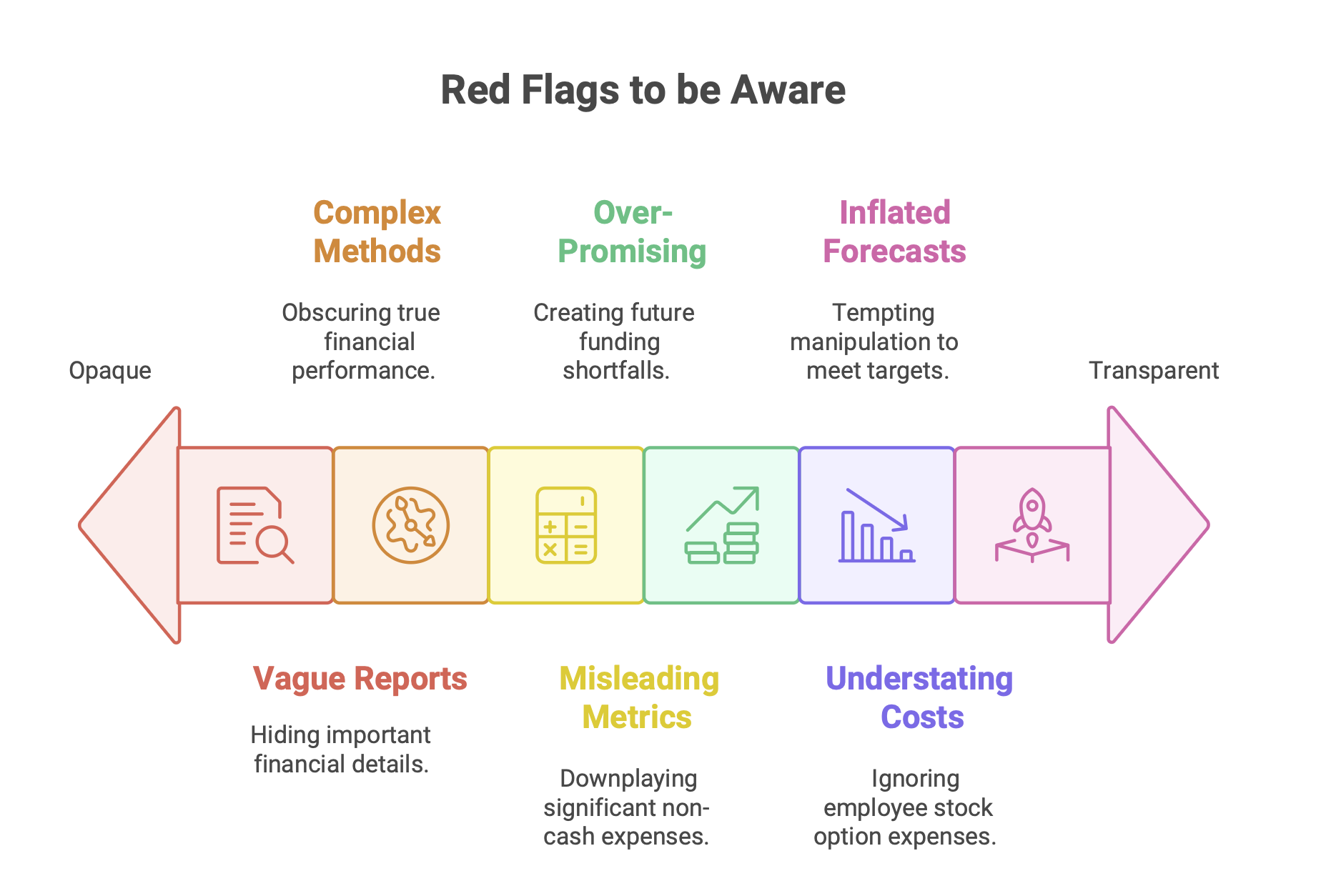

Red Flags: Companies to Be Wary Of

It’s just as important to know what to avoid as what to look for. Steer clear of firms that don't seem to be playing fair with their numbers.

Avoid Companies That:

- Don't account for ESOPs properly: If they give out stock options to employees (ESOPs) but don’t treat it as a real expense, they are understating their costs.

- **Have unrealistic pension assumptions:**If their pension promises seem too good to be true given their funding, it might cause problems later.

- **Use "fancy" accounting:**Overly complex accounting can be a way to hide things. Simpler is often better and more transparent.

- Overly focus on EBIDTA: Especially if they say non-cash expenses (like depreciation) have already been "paid for." These are real costs.

- Lack clear footnotes in financial reports: Footnotes explain the numbers. If they are vague or missing, they might be hiding something.

- Sell overly optimistic projections: No one can predict the future with perfect accuracy. Companies that constantly push super-high growth numbers might be tempted to manipulate results to meet those projections.

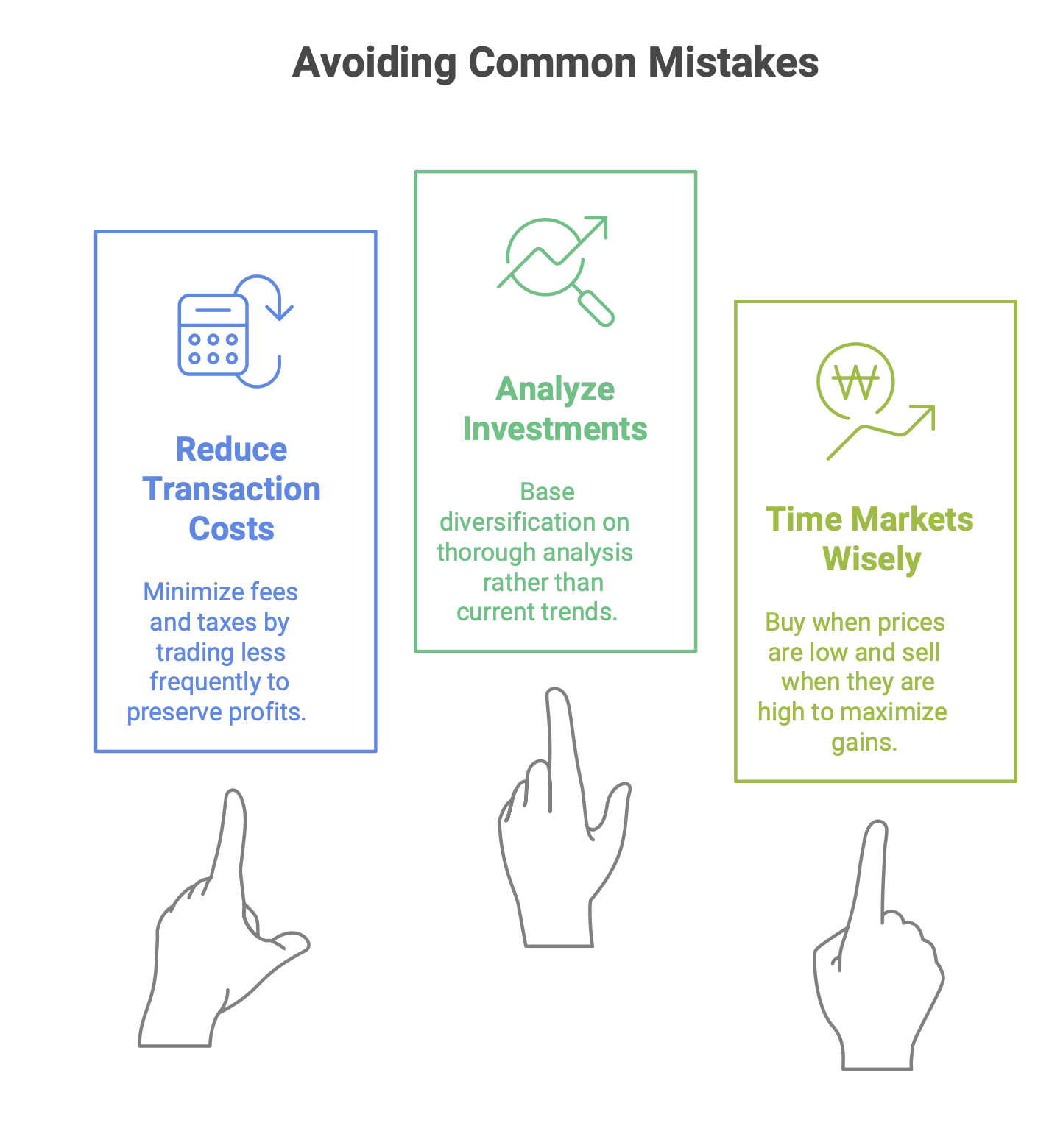

Common Money-Losing Mistakes

Why do some folks end up losing money or not making as much as they could? Here are a few common reasons:

- High Transaction Costs: Trading too much (buying and selling frequently) racks up fees and taxes, eating into your profits.

- Fad-Based Diversification: Spreading your money around based on what's currently popular, rather than on solid analysis of each investment.

- Market Timing Mistakes: This is a classic! Jumping into the market when it’s high (because of FOMO – Fear Of Missing Out) and selling when it’s low (because of panic). This is the opposite of "buy low, sell high."

Keep It Simple

In investing, complexity is often your enemy.

- Simple Propositions Win: A strategy with a single, clear variable for success often has a high chance of working (say, 90%). A strategy dependent on ten different variables all lining up? The chance of success drops dramatically (around 35%).

- Multi-linked chains of events or dependencies create more points of failure. Think simple.

The Quiet Winner: The Passive Investor

In the long run, an investor who makes thoughtful choices and then largely stays put (a passive investor) often earns more. Why? Mainly due to lower transaction expenses. Less tinkering means fewer fees.

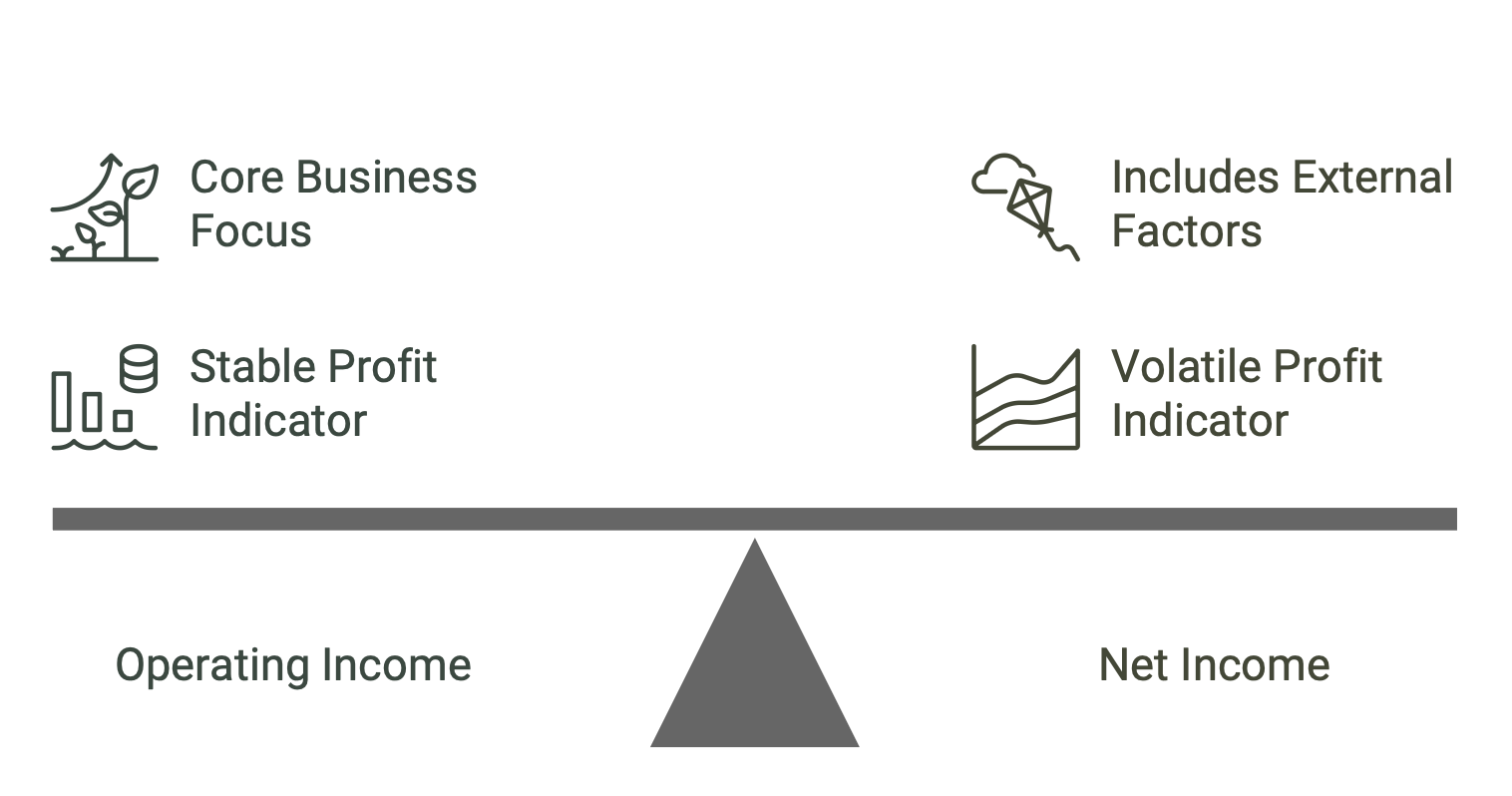

Understanding Company Earnings: Operating Income vs. Net Income

When you look at a company's profits, operating income can give you a better understanding of its core business health than net income.

- Operating Income: Profit from the company's main business operations.

- Net Income: Can include gains or losses from things outside its main business, such as investments in securities. These can be volatile and don't always reflect the core strength.

Share Repurchases: Another Look

We talked about share repurchases. Treat a company's decision to repurchase shares like any new investment decision it might make.

- It’s a good economic idea for a company to buy back its shares when the price is low. Existing shareholders benefit because their stake in the company effectively increases, and they retain more of the company's future earnings.

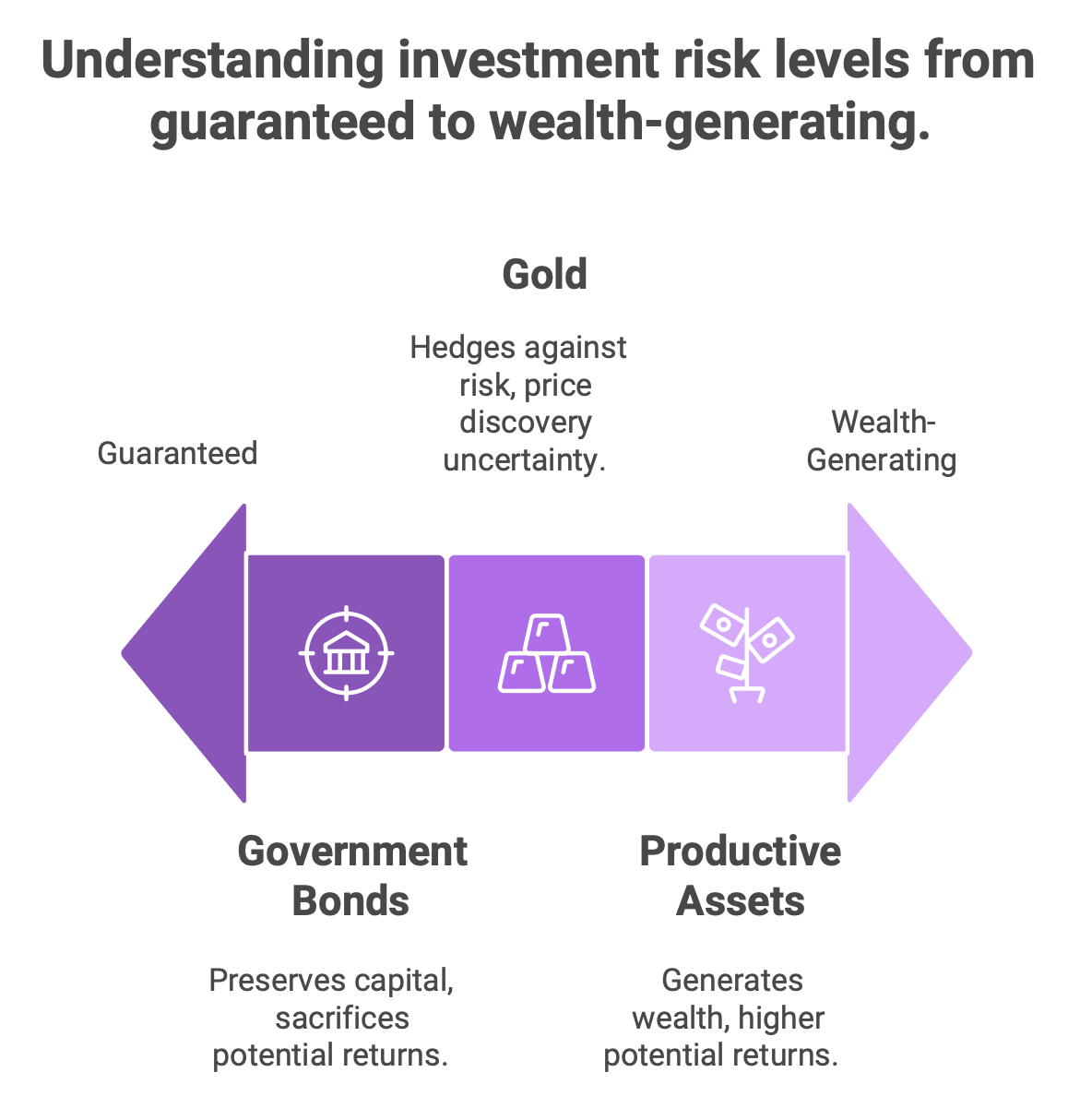

"Risk-Free" Investments: Are They Truly Risk-Free?

You’ll hear about "risk-free" investments such as government bonds or Bank’s FD . But how risk-free are they really?

- If they are returning less than the rate of inflation, you are actually losing purchasing power over time. You’ve given up the ability to use that money now, and in the future, it will buy you less.

- Such investments should mainly be for liquidity concerns (i.e., you need to keep some cash safe and easily accessible).

Focus on Productive Assets

Some assets don’t produce anything on their own but are bought with the hope that someone in the future will pay more for them. Gold is a common example. People often rush to assets like gold or so-called risk-free investments out of fear.

- Instead, try to focus your investments on productive assets. These are things that generate wealth and returns on their own. Think businesses, farms, or commercial real estate that produces rent. These assets work for you.

- Gold price is heavily dependent on Geopolitical situation and movements by Central banks. Hence in the short or medium term, its hard to make clear predictions due to numerous factors at play. I invest in Gold ETF’s to hedge against equity risk but keep it limited due to numerous uncertainty in its price discovery

A Quick Financial Health Check: Interest Coverage

A handy ratio to understand if a company can comfortably pay the interest on its debts is the Interest Coverage Ratio.

- Interest Coverage = Pre-Tax Earnings / Interest Expense.

- A higher number is generally better, indicating the company earns much more than it needs to cover its interest payments. (Sometimes EBIDTA is used in the denominator, but Pre-Tax Earnings is a more conservative measure).

The Golden Rule of Value Investing (Again!)

It’s worth repeating because it’s so important:

It's far better to buy a wonderful business at a fair price than a fair business at a wonderful price.

Quality matters, often more than just a cheap price tag.

PBT over EBIDTA

When looking at profitability, Pre-Tax Profit (PBT) is often a more reliable metric for investment decisions than EBIDTA (Earnings Before Interest, Taxes, Depreciation, and Amortization). EBIDTA can sometimes make a company look healthier than it is by ignoring real expenses such as depreciation and interest charges

The Path to Stable Returns

For stable, long-term returns, the formula is surprisingly straightforward:

- Focus on what you know: Invest in businesses and industries you can understand.

- Take a simple approach: Don't get suckered into overly complex strategies.

- Avoid "get rich quick" schemes: They rarely work and often lead to losses. Slow and steady usually wins the race.

Future Earnings Power: The Real Driver

When you invest, you're buying a share of an asset’s future ability to generate returns.

- If you can't reasonably estimate that future earning power, it’s probably best to pass on that investment.

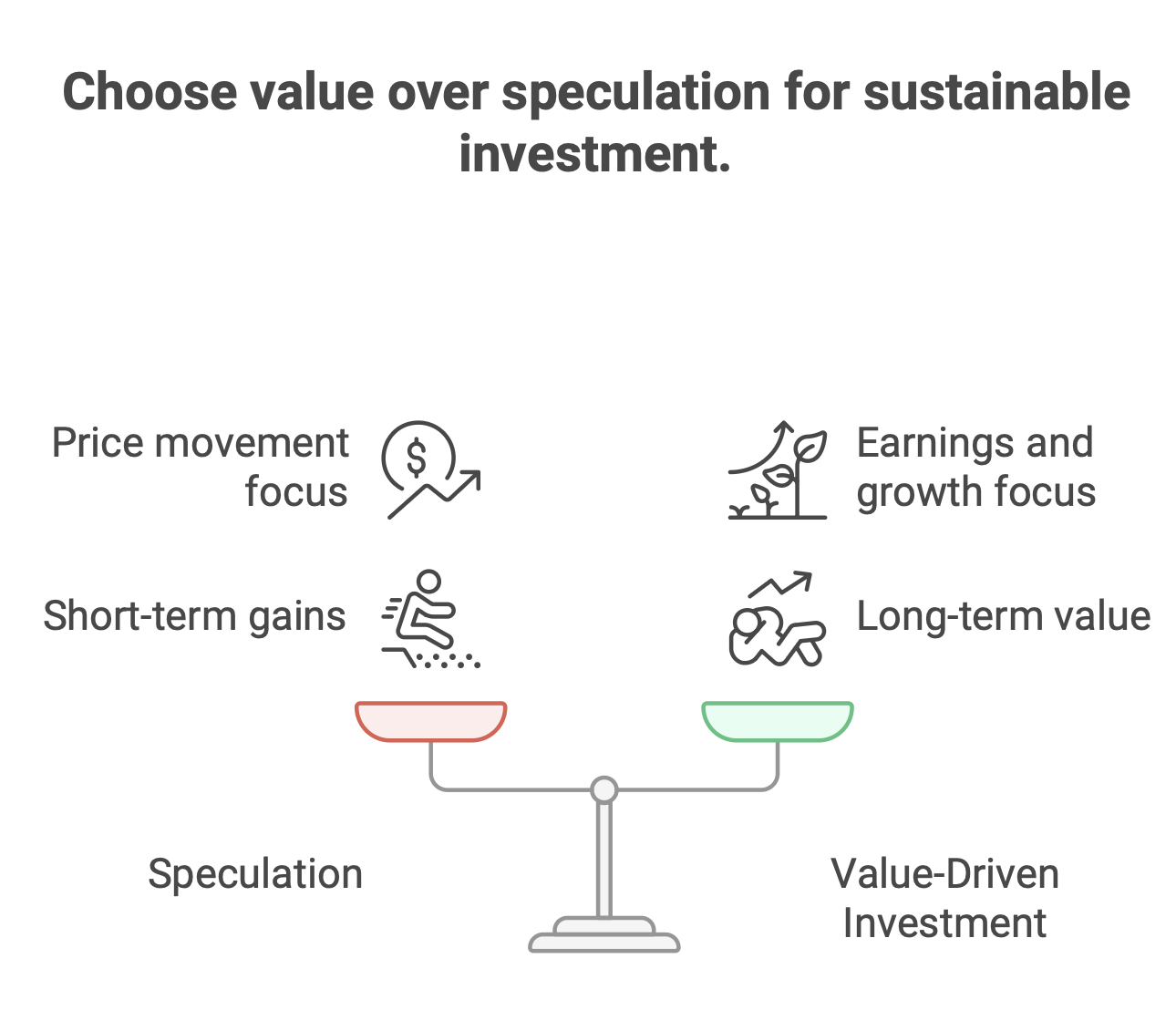

- Don't invest just because you think the price will go up. That's speculation, not investing. Price changes should be a result of the business performing well and generating value, not the primary reason for your investment.

- Past performance (how much an asset’s price has gone up) should never be the only reason to invest. The future can be very different from the past.

Watch the Field, Not Just the Scoreboard

Focus on what your investment is producing – its earnings, its growth, its dividends –rather than solely its daily price movements on the stock market.

- Good players focus on playing the game well (the company focusing on its business), not just constantly looking at the scoreboard (the daily stock price).

- When investing, understand the value your asset is creating. If an asset is genuinely valuable and provides a needed product or service, it will likely be used and generate returns even during tough economic times such as a recession.

Own a Piece of the Business

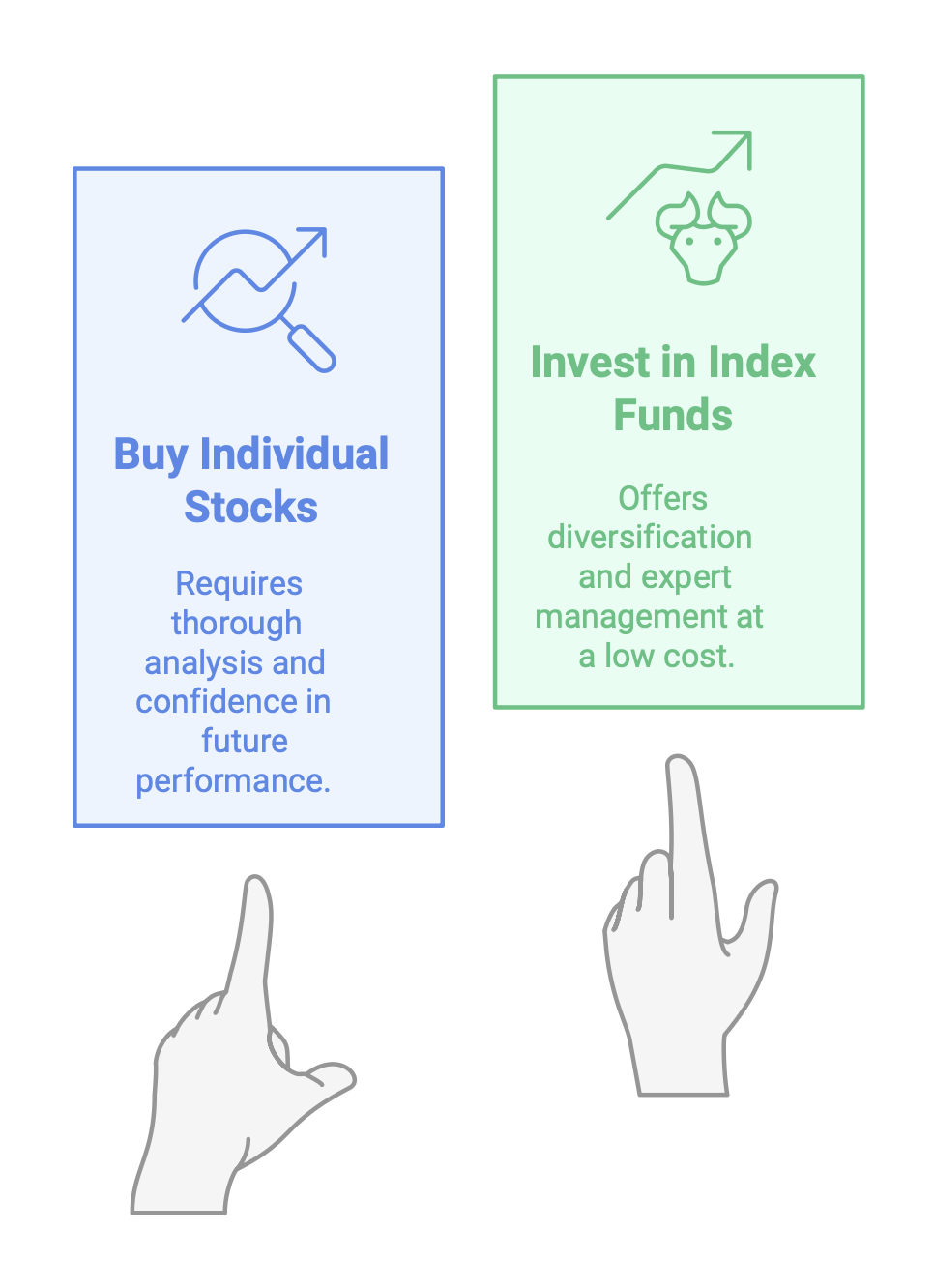

Think of buying a stock as becoming a part-owner of that business, even if it’s a tiny part.

- Analyze it as if you were buying the whole business for yourself.

- Try to estimate its performance for the next 5 years based on the information available. If you can’t do this with some level of confidence, it’s better to avoid it.

- For many people, Index Funds can be a great option. With an index fund, you're buying a basket of stocks that mimics a market index (such the Nifty 50 or Sensex). Experts often manage these, and they are generally under high scrutiny, offering diversification at a low cost. Most of my equity investments over the past decade has been in Index funds and keeps my process super simple.

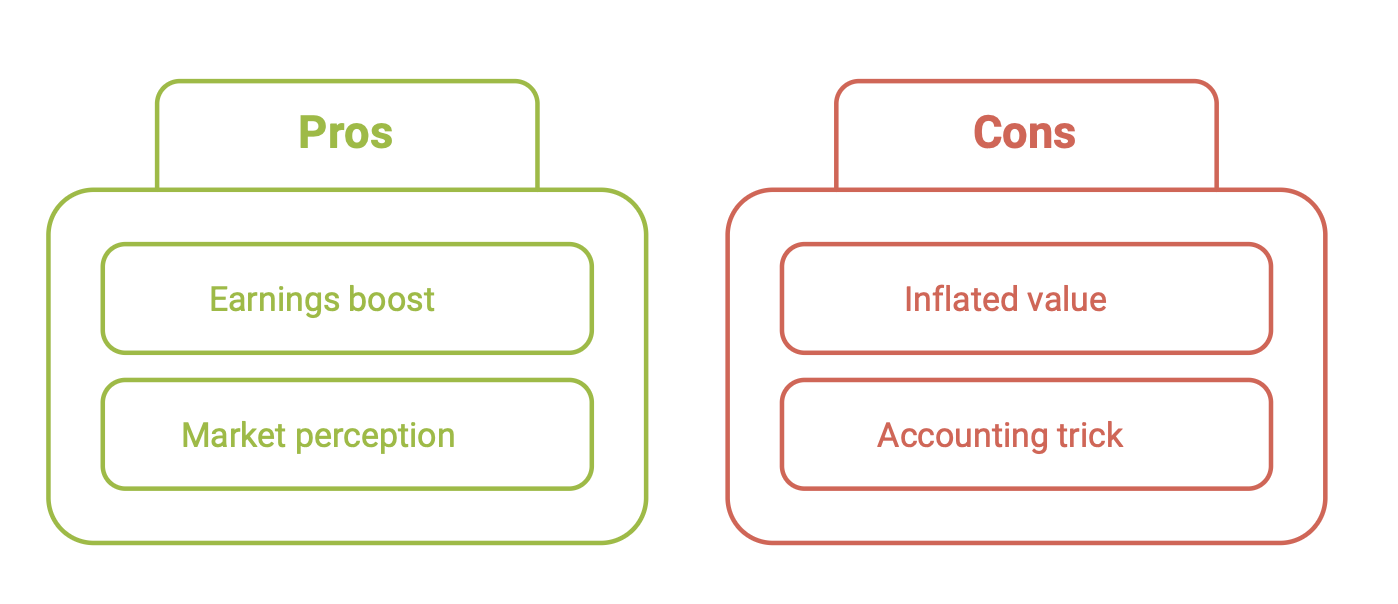

The P/E Game in Acquisitions

Sometimes, large organizations buy smaller firms that have a low Price-to-Earnings (P/E) ratio. They then pool the earnings of this acquired firm with their own larger earnings. This can sometimes make it look like the acquired firm's value has suddenly increased more than it organically has, simply because it's now part of a larger, perhaps more favorably valued entity. It's an accounting and perception play to be aware of.

When Good Investments Turn Bad

Even a fundamentally sound investment can turn into a risky speculation if you buy it at a super high price. The price you pay matters immensely. Overpaying can erase the benefits of picking a good company.

A Strict No: Borrowed Money

Always bear in mind. Borrowed money (leverage or margin) has no place in an ordinary investor’s toolkit. If the market goes against you, borrowing can magnify your losses significantly and can even wipe you out. Invest what you can afford to lose or see go down in value temporarily.

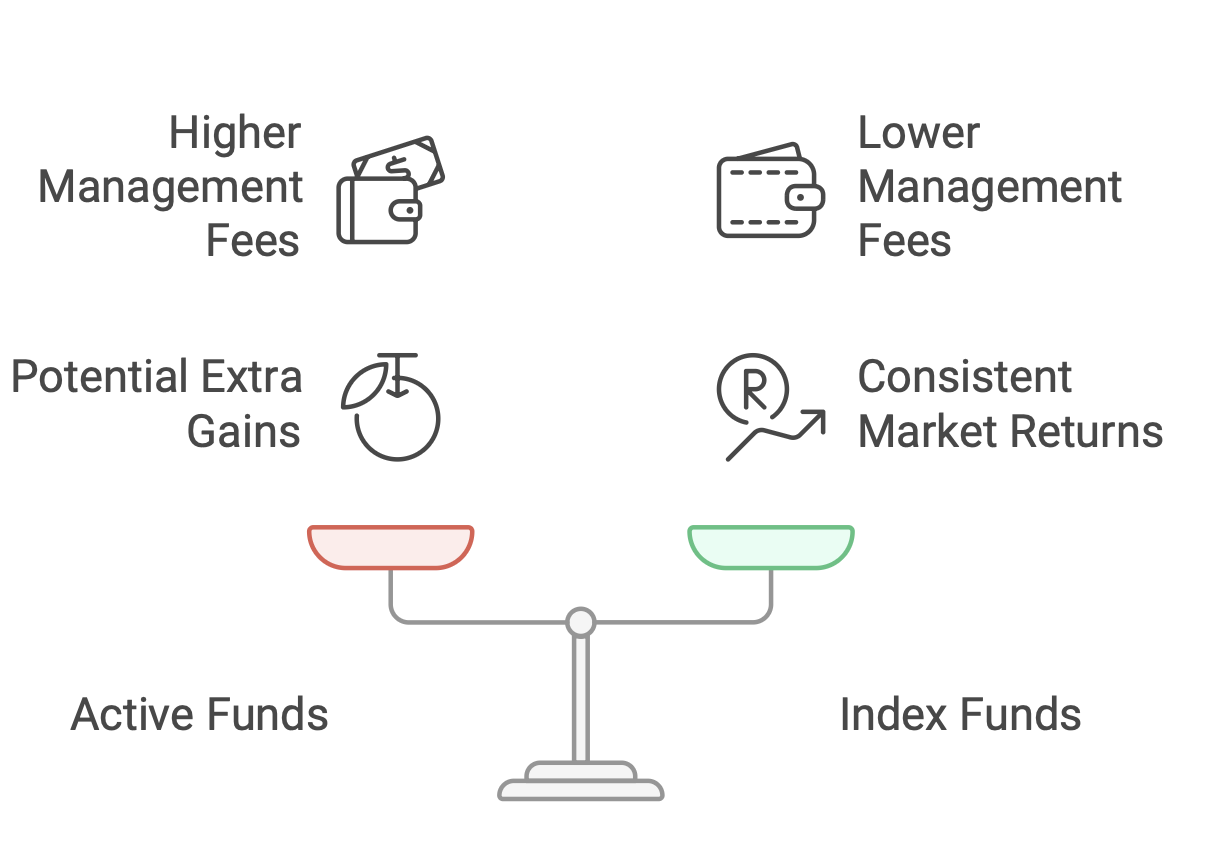

The Hidden Costs of Active Funds

Many actively managed mutual funds (where a fund manager tries to pick winning stocks) often have higher fees.

- In many cases, any extra gains these active funds might make (compared to a simple index fund) are eaten up by these management fees and transaction costs from frequent trading. Sometimes, these fees can take away all the extra performance, and then some more

Conclusion: Your Investing Journey

Anyone starting anew may find it a bit too complicated. However, don't feel overwhelmed. Investing is a journey, not a race. Start with these foundational ideas, focus on learning, be patient, and think for the long term.

You’re not just investing money; you’re investing in your future self. The key is to start, stay disciplined, and keep learning.